🎓 GAAP vs Non-GAAP: What Investors Overlook in Earnings

The type of earnings you use can lead to the wrong conclusions.

Many investors look ahead to decide if a stock is cheap or expensive. To do that, they use the forward P/E ratio, and based on that number, they conclude if a stock is cheap or expensive. But here’s the problem: not all earnings are the same.

Companies can report different versions of earnings, and the difference between them can be significant. That means a stock that looks cheap can actually be much more expensive. And that has a direct impact on valuation.

That’s why it’s so important to understand which earnings you’re using when valuing a company, and how they can lead to very different valuations.

In this article, we’ll break down the two types of earnings: GAAP and non-GAAP.

You’ll learn:

📊 what the key differences are between GAAP and non-GAAP

🧾 what is included (and what is excluded)

🎯 how they impact valuation

We’ll also use a real-world example to show how big the difference can be.

Let’s start with GAAP, the official way companies report earnings.

📊 What is GAAP?

GAAP stands for Generally Accepted Accounting Principles. It’s the industry standard for reporting financial results, which makes companies comparable. These are the numbers you’ll find in their income statements.

GAAP includes all costs. That means the following is included:

operating expenses

interest and taxes

stock-based compensation

restructuring and other charges

These are all costs related to running the business. Nothing is excluded, which means GAAP reflects the full financial picture of a company’s performance.

GAAP earnings show what a company actually earned over a period. There are no adjustments, no “cleaned” numbers, and no exclusions to make results look better. It reflects the true bottom line.

Because GAAP includes everything, earnings can sometimes look lower, especially in the short term. One-time charges, restructuring costs, or acquisition-related expenses can impact results in a given quarter or year. That doesn’t always mean the underlying business is weaker.

If you want to understand a company’s profitability, GAAP is your starting point. It shows what is actually reported and what shareholders are left with. But GAAP doesn’t tell the whole story about how a business is performing. That’s where non-GAAP comes in.

📊 What is Non-GAAP?

Non-GAAP earnings are adjusted numbers. Companies start with their GAAP results and then exclude costs. These are costs such as:

stock-based compensation

restructuring costs

acquisition-related expenses

other “one-time” items

The goal is to show a clearer view of the underlying business. One example of a non-GAAP metric is EBITDA, which excludes interest, taxes, depreciation and amortization. This allows non-GAAP to focus more on the core performance.

Unlike GAAP, non-GAAP is not standardized. Companies decide what they exclude and how they present these numbers, which means results are not always comparable.

Non-GAAP is a useful way to understand how a business is performing without short-term impact. However, it’s important to be careful. Some of the costs that are excluded are not always one-time. Stock-based compensation, for example, is often excluded, while it is a recurring cost for many companies. This can make earnings look higher than they are.

Non-GAAP can help you understand the business, but it doesn’t always show the full picture when valuing a company.

Source: The Motley Fool

🔥 Upgrade Now & Save 30%

Get full access to our Portfolios & Transactions, our Best Buys, all Deep Dives, all Stock Battles — plus 375+ premium articles to explore!

✅ Join 4,500+ investors already inside.

🎯 The Impact on Valuation

Most investors use the forward P/E ratio to value a company, meaning they look at expected future earnings. But here’s the problem: the “E” in that ratio is often based on non-GAAP EPS.

As discussed earlier, this means costs such as stock-based compensation, restructuring costs, and acquisition-related expenses are excluded. As a result, the EPS used in the forward P/E is often higher than the actual EPS, which leads to a lower P/E ratio.

For example, a stock might trade at a forward P/E of 25, which at first glance can look reasonable. However, that multiple is based on non-GAAP EPS. If you instead look at GAAP EPS, those costs are included, which usually results in lower earnings, especially for growth companies where stock-based compensation can be significant.

The same stock trading at 25x non-GAAP EPS might actually trade at 40x or more based on GAAP EPS. It’s the same company and the same business, but a very different valuation.

This is where many investors get it wrong, and it’s not just theory. Let’s look at a real example: Axon Enterprise.

🛡️ Example: Axon Enterprise

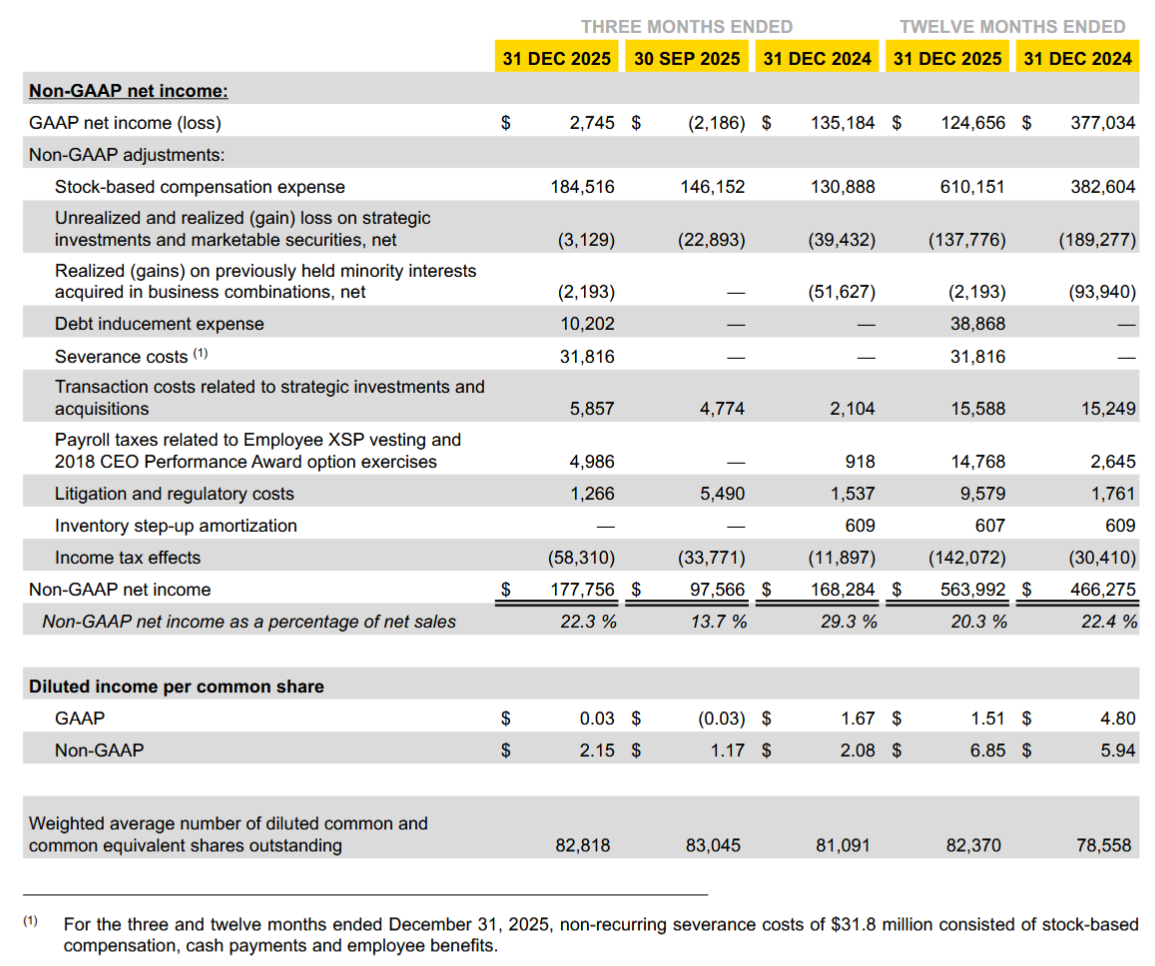

The difference between GAAP and non-GAAP can have a big impact on valuation. You often see this with high-growth companies. Let’s take Axon as an example.

As you can see in the image below, for Q4 2025, Axon reported a non-GAAP net income of $177.8 million and an EPS of $2.15. But on a GAAP basis, net income was just $2.7 million, with EPS of only $0.03.

The biggest impact comes from stock-based compensation, which was $184.5 million in the quarter. This has a major impact on reported earnings and brings net income close to zero.

So GAAP EPS is much lower than non-GAAP EPS, and that’s exactly the point, because GAAP EPS is the actual “E” used in the trailing (TTM) P/E ratio.

Source: Q4 2025 Axon Enterprise Shareholder Letter

At the current share price of $402.85 and a GAAP EPS of $1.51, Axon trades at a P/E ratio of 267.

If we look, like many investors do, at Axon’s forward P/E ratio for 2026, it is 51.7 (source: GuruFocus). At first, that may look reasonable. You might think earnings will grow quickly and the valuation will come down next year. But here’s the problem: that 51.7 is based on non-GAAP EPS of 7.79, which means costs are excluded. And we know that can have a big impact on the valuation.

The expected GAAP EPS for 2026 is 1.68. Based on that, the real forward P/E at the current stock price would be around 240.

Still very high, and very different from what the forward P/E shows.

📌 Final Takeaway

Not all earnings are the same. GAAP shows the full picture. Non-GAAP shows a cleaner version of the business. Both matter, but for different reasons.

If you want to understand how a business is performing, non-GAAP helps.

If you want to value a company, GAAP matters most.

Make sure you understand the numbers and use the right earnings. Otherwise, you risk reaching the wrong conclusions, and making the wrong decisions. Good luck!

Thank you for reading! 🙏

We put a lot of love into creating this post for you. If you enjoyed it, feel free to click the ❤️ button so more people can discover it on Substack or hit the ↪️ share button to share it with friends, family and fellow investors!

Don’t hesitate to share your thoughts in the comments — we’d love to hear from you 💬

That’s it for today.

We’ll see you again in the next edition of our newsletter!

Until then, invest wisely.

Vincent & Stefan

The Future Investors

Disclaimer:

The information and opinions provided in this article are for informational and educational purposes only and should not be considered as investment advice or a recommendation to buy, sell, or hold any financial product, security, or asset. The Future Investors does not provide personalized investment advice and is not a licensed financial advisor. Always do your own research before making any investment decisions and consult with a qualified financial professional before making any investment decisions. Please consult the general disclaimer for more details.