Welcome to another edition of Unpacked, our monthly series where we explore a different company in detail. Each month, we break down its story, business model, and highlight the latest developments.

Additionally, we do a detailed fundamental analysis, diving into the company’s management, market, financials, and growth estimates. We score each area separately, leading to a final score between 0 and 100. This score reflects how fundamentally attractive we believe the company is as an investment, ranging from:

🔴 Below 50 → Uninvestable

🟠 50 - 59 → Questionable

🟡 60 - 69 → Reasonable

🟢 70 - 79 → Quality

🔵 80 - 89 → High-Quality

🟣 90 or above → Exceptional

The goal? To give you a full deep dive into this company, as a complement to your own research, so you can decide if it’s the right investment for you.

In case you missed it, here you can read the previous edition of Unpacked:

In our second Unpacked, we’re taking a closer look at AppLovin, a name that may be unfamiliar to many, but one that has been growing rapidly in recent years. AppLovin is a fast-growing player in the mobile app industry, known for its platform that helps app developers reach a larger audience and maximize their revenue. Through smart acquisitions and a strong focus on technology, AppLovin has positioned itself as a key player in the mobile app space.

What sets AppLovin apart? Is it the potential for scale, the tech they bring to the table, or their approach to quick expansion? And the key question — is AppLovin a smart pick for your portfolio?

Now let’s unpack the fundamentals of this growing company — and check out how we score it!

History and Business Model

AppLovin was founded in 2011 by Adam Foroughi, John Krystynak, and Andrew Karam. The company started as an advertising platform focused at helping mobile app developers grow and monetize their apps. The platform was officially launched in 2012, and from that point on, AppLovin focused on helping developers target the right users through advanced advertising systems.

In the years that followed, AppLovin expanded its operations, becoming an essential tool for many mobile app developers. The company formed strong partnerships with game studios like Lion Studios, Machine Zone, and Belka Games, which led to the expansion of its own portfolio of mobile games. Through these strategic collaborations, AppLovin grew not only as a platform but also developed into a player in the gaming market.

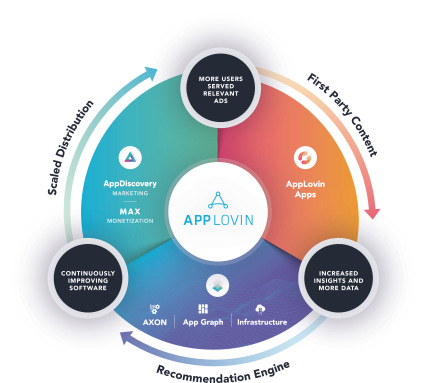

AppLovin’s business model is built around providing an advertising platform that helps app developers make money from their apps. Its AXON technology helps brands improve their ads and reach the right people. This technology uses data and machine learning to make ads work better and increase revenue for developers. Besides making money from ads in apps, AppLovin also provides tools to help developers attract and keep users.

Source: AppLovin IPO Prospectus

The company’s products include:

AppDiscovery: Helps businesses find and attract the right users through targeted ads.

MAX: Helps mobile apps make more money by improving ad revenue.

SparkLabs: Helps create ads that get better results.

AppLovin Exchange: A program that gives businesses access to a wider audience.

Array: Helps businesses get more value from their customers by improving engagement.

Adjust: Offers tools to track and measure marketing efforts.

Wurl: Helps businesses make money from users on streaming TV.

These products work together to help businesses attract users, increase revenue, and improve performance across various channels.

Revenue Breakdown

In 2024, AppLovin brought in a total of $4.71 billion in revenue, split across two main areas:

Advertising (68%): This reflects revenue from AppLovin’s advertising platform, including tools like AppDiscovery, MAX, and ALX, powered by the AI-driven AXON engine. This segment grew with a significant 75% compared to 2023.

Apps (32%): This is the revenue from AppLovin’s mobile apps, mostly games by studios like Lion Studios, through in-app purchases and ads. It grew with a modest 3% increase from last year.

Recent Developments

In recent years, AppLovin has made significant moves to adjust its strategy and focus. Below are the key recent developments:

Focus on AI Technology with AXON 2.0:

AppLovin has further developed and improved its AI-driven advertising platform, AXON 2.0, launched in 2023. This platform has become more efficient in delivering targeted ads, leading to improved performance for advertisers and strong growth in the software platform segment.Strengthening the MAX Advertising Platform

Last year, AppLovin invested over $150 million to acquire specific assets from Zynga’s portfolio, aiming to significantly improve and expand the capabilities of its MAX advertising platform. This strategic acquisition allowed AppLovin to integrate valuable gaming-related resources and technology, further building its position and influence within the gaming advertising marketExpansion into E-Commerce

A significant strategic shift is AppLovin’s entry into the e-commerce sector. The company is starting to focus on providing new advertising opportunities for businesses that sell products online. In Q2 2024, AppLovin launched a pilot program for e-commerce advertising, which showed promising results with nearly 100% incremental lift for advertisers. Analysts expect e-commerce to account for 10% of revenue in 2025 and 16% in 2026, reducing AppLovin’s reliance on mobile gaming and positioning it to compete with companies like Meta.Sale of the Apps Division

Two months ago (February 2025), AppLovin announced plans to sell its Apps (gaming) division for $900 million, with the deal expected to close in Q2 2025. CEO Adam Foroughi stated that the company’s true focus has always been on advertising technology, not game development. This divestment allows AppLovin to shift its focus entirely to advertising, positioning itself to attract a broader range of advertisers and become a key player in the global digital advertising market.Concerns from Research Firms

AppLovin’s stock dropped in late February after negative reports from Fuzzy Panda Research and Culper Research. The reports claimed the company was involved in ad fraud, illegal tracking, and improper data use, saying that AppLovin took advantage of app permissions and collected data without consent. CEO Adam Foroughi quickly responded, calling these claims “false and misleading” and stating that the company follows app store rules. Despite the controversy, most analysts stayed positive, noting that there were no legal issues or fraud concerns in AppLovin’s financial audits.

AppLovin is changing its focus by improving AI, expanding into e-commerce, selling its app development business, and growing its advertising platform through key acquisitions. These moves show its shift toward a larger, more scalable focus on advertising technology.

Fundamental Analysis

In the fundamental analysis, we evaluate three key areas: management, market, and financials & growth estimates. Each area contains multiple elements and each element is scored individually, leading to a final score between 0 and 100.

Final Scoring

This score reflects how fundamentally attractive we believe the company is as an investment, ranging from:

🔴 Below 50 → Uninvestable

🟠 50 - 59 → Questionable

🟡 60 - 69 → Reasonable

🟢 70 - 79 → Quality

🔵 80 - 89 → High-Quality

🟣 90 or above → Exceptional

Unlock our scoring framework and full fundamental analysis below, and see how we score AppLovin on a scale from 0 to 100 — exclusively available to our paid members! 🚀